Let's embark on the journey of how it all started

Our pledge to excellence in providing personalized mortgage solutions for your unique path to financial success and homeownership.

Get in touch

Our Story

The Ridge Mortgage is a private wealth mortgage banking firm built for high-performing real estate professionals, builders, and borrowers who demand more than a traditional lending experience.We combine decades of industry expertise with boutique-level execution and institutional-grade pricing power.We operate outside the traditional retail mortgage model. That means more flexibility, stronger pricing control, and the ability to structure loans around the borrower—not force borrowers into rigid boxes. Our approach is simple:

Better pricing. Cleaner execution. Faster closings.

14 days

Avg. Closing Time

20+

5 star reviews

27+

Years of mortgage experience

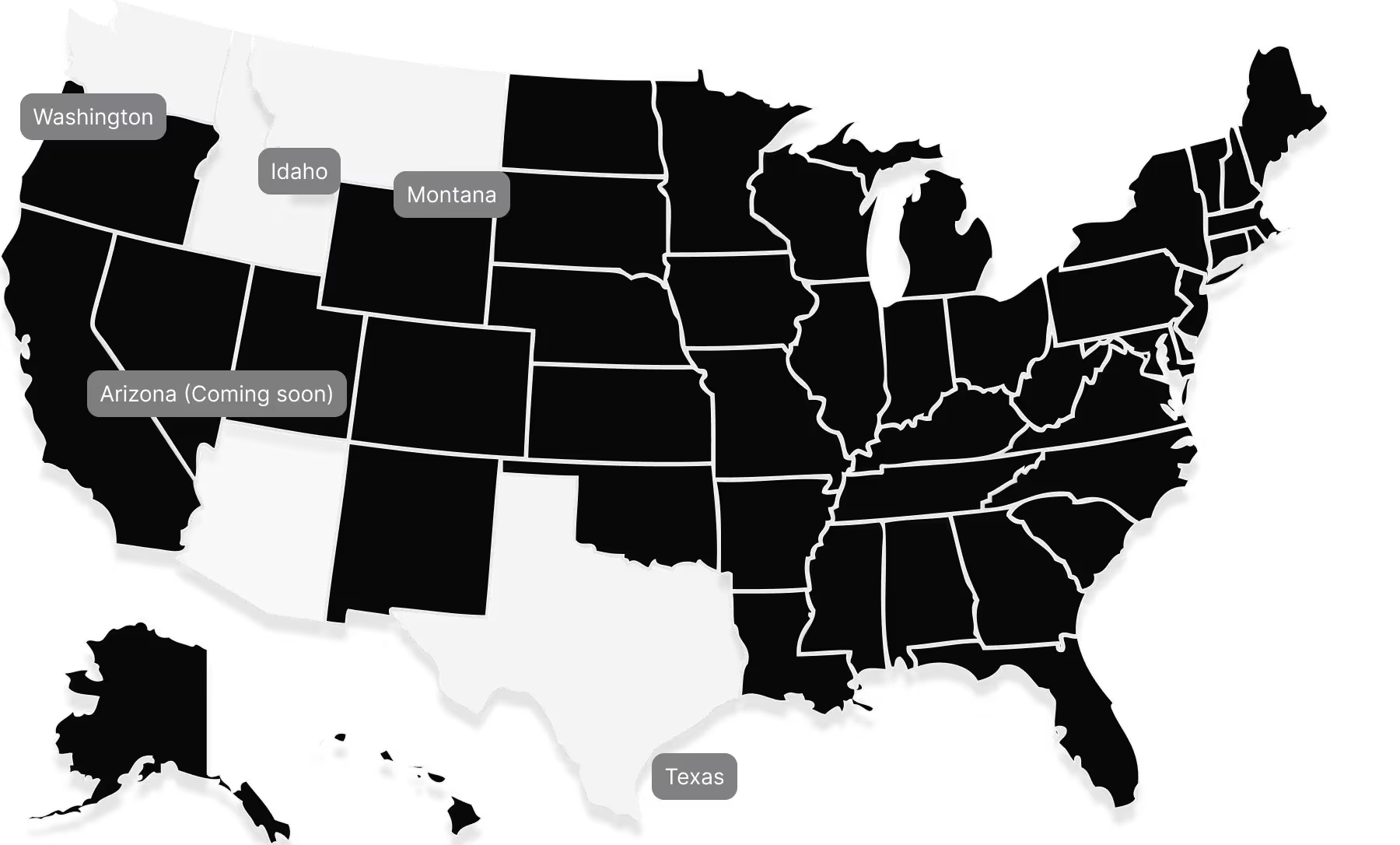

Licensed in 4 states currently

Our simple home loan process

Pre-Approval

Before house hunting, potential buyers should get pre-approved for a mortgage. This involves submitting financial information to a lender who then evaluates credit history, income, debts, and assets to determine your loan terms.

Loan Application

Once pre-approved, buyers can start looking for a home within their budget. After finding a property and agreeing on the price, they formally apply for a mortgage. This step requires updated detailed financials and documentation.

Lock Rate

When you lock in a rate, you and the lender agree to a specific interest rate for your mortgage. This rate remains unchanged irrespective of market fluctuations during the lock period. The lock-in period usually ranges from 15 to 60 days.

Loan Processing

The lender processes the application, which includes verifying all the information provided by the applicant. They may request additional documents or clarification. During this stage, an appraisal of the property is also conducted to assess its market value.

Underwriting

In this critical phase, the underwriter reviews all documentation and decides whether to approve or deny the loan based on criteria like credit score, debt-to-income ratio, and property value. This is where the lender takes on the financial risk of the loan.

Closing

The final step is closing. This involves signing a variety documents that finalize the mortgage process. The buyer typically pays the closing costs, and the ownership of the property is transferred. Once this is completed, the buyer is now the new owner of the home!